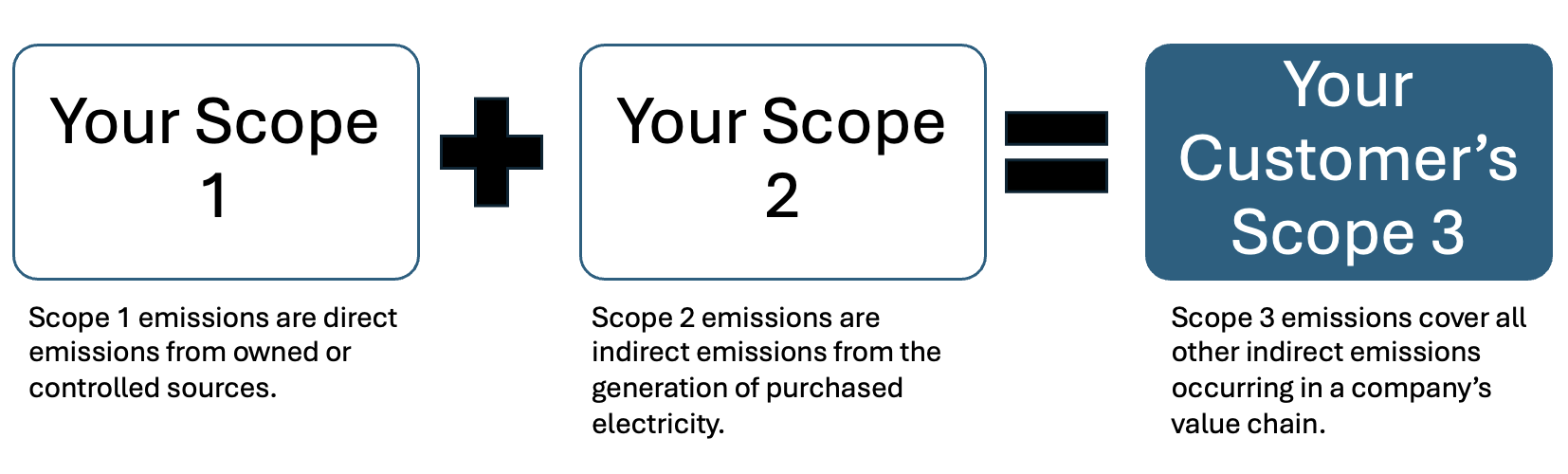

What Is Scope 3?

SBTi’s draft Corporate Net‑Zero Standard V2 strengthens supply‑chain accountability. Here’s what’s changing, why it matters for your ESG program and solutions, and how you can prepare.

Scope 3 includes all indirect GHG emissions that occur in a company’s value chain, both upstream and downstream. It often makes up the largest share of a company’s total carbon footprint.

Scope 3 Categories (GHG Protocol)

| # | Category | Description |

|---|---|---|

| 1 | Purchased goods & services | Cradle‑to‑gate emissions from the extraction, production and transport of goods and services purchased by the reporting company. |

| 2 | Capital goods | Emissions from the production of capitalized goods (e.g., buildings, machinery, vehicles) acquired by the company. |

| 3 | Fuel‑ and energy‑related activities (not in Scopes 1 or 2) | Upstream emissions related to fuels and electricity purchased and consumed (e.g., extraction, production and transmission losses). |

| 4 | Upstream transportation & distribution | Third‑party transportation and warehousing of purchased products between suppliers and the reporting company. |

| 5 | Waste generated in operations | Emissions from third‑party disposal and treatment of waste generated by the company’s operations. |

| 6 | Business travel | Transportation of employees for business‑related activities in vehicles not owned or controlled by the company. |

| 7 | Employee commuting | Transportation of employees between their homes and worksites. |

| 8 | Upstream leased assets | Operation of assets leased by the company (upstream) not included in Scopes 1 and 2. |

| 9 | Downstream transportation & distribution | Transportation and distribution of sold products in vehicles and facilities not owned or controlled by the company, including retail and warehousing. |

| 10 | Processing of sold products | Emissions from processing of intermediate products sold by the company by third parties. |

| 11 | Use of sold products | Direct use‑phase emissions from goods and services sold by the company. |

| 12 | End‑of‑life treatment of sold products | Waste disposal and treatment of products sold at end of life. |

| 13 | Downstream leased assets | Operation of assets owned by the reporting company and leased to other entities. |

| 14 | Franchises | Operation of franchises not included in Scopes 1 and 2 of the franchisor. |

| 15 | Investments | Emissions from equity and debt investments and project finance; primary category for financial institutions. |

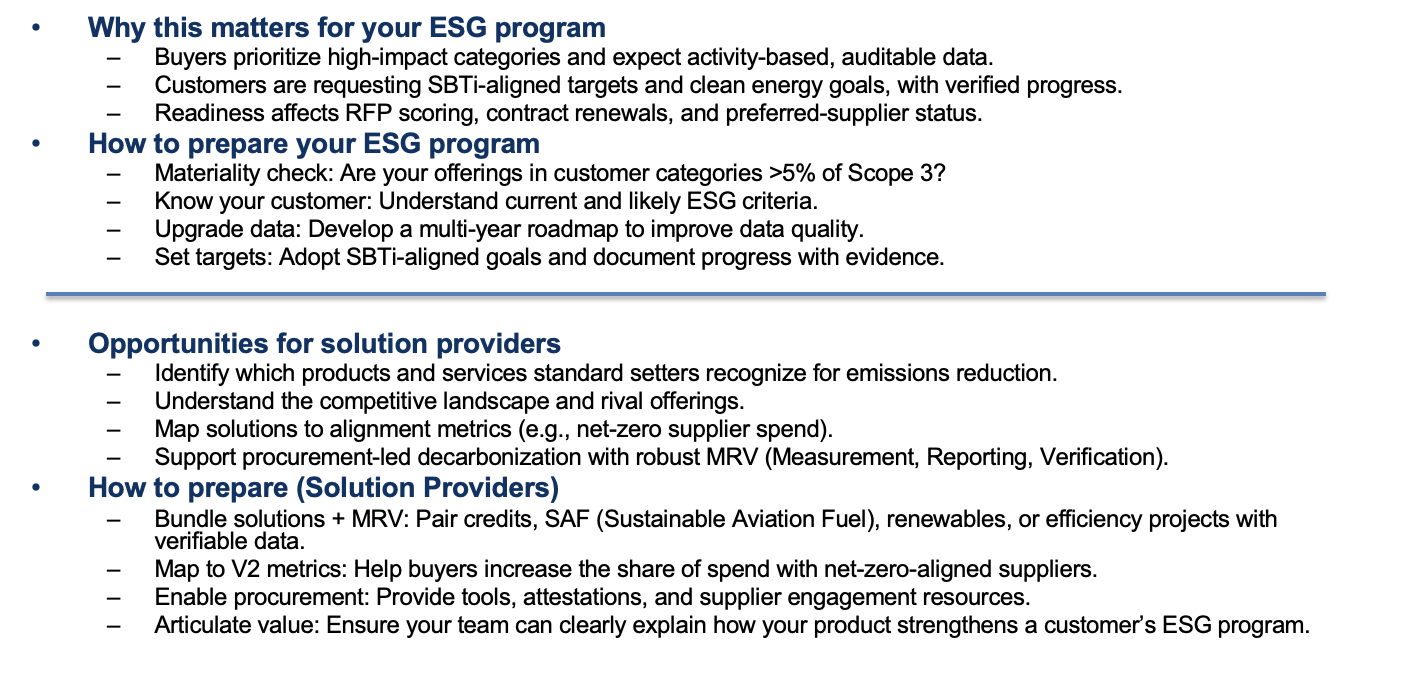

Why this matters to you

What’s changing in SBTi V2 (Draft, Mar 2025)

| Feature | Current (V1) | Proposed (V2 Draft) | Source |

|---|---|---|---|

| Scope 3 boundary | Broader discretion across 15 categories | Materiality‑based: disclose categories contributing > 5% of total Scope 3 or where influence is greatest | SBTi |

| Supplier engagement | Encouraged | Where Scope 3 > 40% of total, buyers must engage suppliers covering ≥ 67% of relevant emissions | SBTi |

| Data quality | No multi‑year plan required | Companies implement multi‑year supplier data‑quality roadmaps | SBTi |

| Alignment metrics | Reduction‑only emphasis | New metrics incl. % procurement with net‑zero–aligned suppliers & % revenue from net‑zero products/services | SBTi |

See also SBTi’s overview page: Developing the Corporate Net‑Zero Standard V2.

Turn compliance into an advantage

Early movers will convert supply‑chain transparency into strategic resilience. Need help tailoring this for your suppliers or product team?

References

- SBTi – Draft Corporate Net‑Zero Standard V2 Explained (blog)

- SBTi – Corporate Net‑Zero Standard V2 Consultation Draft (PDF)

- GHG Protocol – Technical Guidance for Calculating Scope 3 Emissions (Full PDF)

- SBTi – Developing the Corporate Net‑Zero Standard V2 (overview)

- GHG Protocol – Scope 3 Calculation Guidance Overview